The catering world runs on card payments. Corporate clients paying $8,000 for a conference lunch, wedding parties dropping $15,000 deposits, holiday party coordinators swiping company cards for $3,500 buffets — processing fees eat into every single transaction. So when a federal judge approved the preliminary Visa/Mastercard settlement that cuts interchange fees by roughly 0.1%, caterers handling hundreds of events annually should be paying close attention to what this actually means for their margins.

Most catering operations have payment workflows built around the old fee structures. Booking systems, deposit policies, invoicing rules, even menu pricing — all of it assumes certain payment costs. A seemingly tiny fee reduction multiplied across an entire event calendar creates ripple effects that most caterers aren't set up to capture.

The settlement also changes surcharging rules, letting merchants add fees or offer cash discounts more transparently. For caterers who've been quietly absorbing 2.5% to 3% in processing costs on every invoice, this opens up pricing strategies that weren't really viable before. Rolling out those changes without alienating corporate clients or confusing wedding planners takes some actual planning, though.

The hidden math of catering payment costs

Take a mid-sized catering operation running around 180 events per year — a mix of corporate lunches, wedding receptions, and private parties, average ticket somewhere around $4,800. That's roughly $864,000 in annual revenue flowing through card payments.

-

Standard interchange

2.2% to 2.9% depending on card type

-

Processing markup

0.15% to 0.5%

-

Monthly fees

$30 to $150

-

Per-transaction fees

$0.10 to $0.30

Total damage? Somewhere between $21,000 and $28,000 annually. That's roughly an entire part-time staff member's salary disappearing into transaction fees.

Now think about how catering payments actually work. Unlike restaurants with small, frequent transactions, caterers deal with:

-

Large deposits collected months in advance

-

Final payments due days before events

-

Add-on charges for last-minute guest count increases

-

Partial refunds for weather cancellations

-

Split payments across multiple corporate departments

Each of those carries a different fee structure. Corporate cards cost more than debit cards. American Express still runs higher than Visa/Mastercard. International cards add currency conversion on top. The complexity means most caterers have no real idea what their effective payment rate actually is — they just see a monthly fee total and move on.

Why traditional payment tracking fails caterers

Standard accounting software treats payment processing as a single expense line. You see "$2,100 in processing fees" for the month, and that tells you essentially nothing about which events, which payment methods, or which client types are actually costing you the most.

End chaos with centralized catering management.

Caterngly helps you plan, confirm, and manage every catering event seamlessly.

- Unified event and order management

- Real-time client updates

- Staff and resource scheduling

No credit card required

Without that breakdown, you can't answer basic questions like:

-

Do wedding clients cost more in fees than corporate accounts?

-

Should we be pushing ACH transfers for deposits over $5,000?

-

Are we actually losing money on small add-on charges?

-

Which events should absorb fees versus pass them through?

The swipe fee settlement makes this kind of tracking more important, not less. When fees drop by 0.1%, that savings gets buried in monthly statements unless you're actively watching effective rates per transaction type. You need visibility into exactly where those savings show up — and right now, most caterers don't have it.

This connects directly to broader margin tracking — something worth reading about in our post on building catering KPI dashboards. Payment processing is just one piece of per-event profitability, but it tends to be the most ignored.

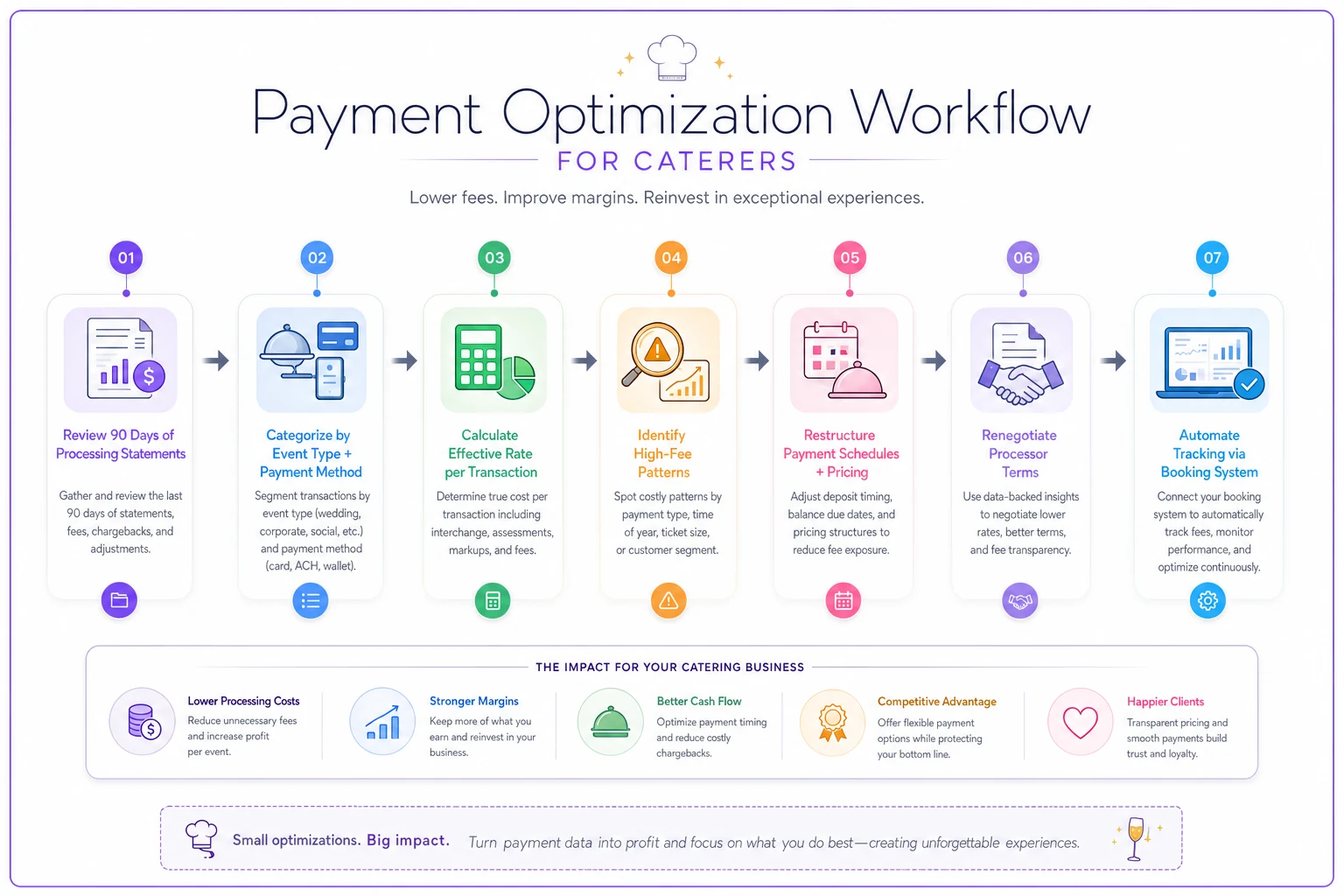

The 6 operational moves to implement now

Here's how the payment optimization process should flow once you've decided to get serious about it:

-

Review 90 Days of Processing Statements

-

Categorize by Event Type + Payment Method

-

Calculate Effective Rate per Transaction

-

Identify High-Fee Patterns

-

Restructure Payment Schedules + Pricing

-

Renegotiate Processor Terms

-

Automate Tracking via Booking System

The diagram below summarizes that flow and where automation typically adds value.

1. Rebuild your payment cost tracking

Stop treating processing fees as general overhead. Start allocating them to specific events and client types.

Add fields in your booking system for:

-

Payment method used

-

Transaction amount

-

Processing fee charged

-

Effective rate (fee ÷ amount)

-

Client type (corporate/social/nonprofit)

Pull three months of processing statements and backfill this data. Patterns show up faster than you'd expect — maybe corporate clients always pull out high-fee company cards, or wedding deposits cluster around amounts that trigger higher interchange tiers. You won't know until you look.

2. Restructure deposit and payment schedules

Large transactions cost more in absolute dollars even at lower percentage rates. A $10,000 wedding payment at 2.5% costs $250. Two $5,000 payments might qualify for lower interchange tiers, saving $15 to $20 per event — not life-changing on a single booking, but meaningful across 50 or 60 weddings a year.

Consider testing a split payment structure:

-

30% deposit at booking

-

40% payment 30 days out

-

30% final payment week of event

This also improves cash flow and reduces refund exposure. Just make sure your contracts spell out the schedule clearly before you start rolling it out.

3. Implement transparent fee pass-through options

The settlement's surcharging changes mean you can be more upfront about payment costs. The trick is doing it without killing bookings.

Instead of tacking on surprise fees at checkout, build two pricing options into your proposals:

-

Cash/ACH price (base rate)

-

Card price (2.5% higher)

"Frame it as a discount for cash/ACH rather than a penalty for cards. \"Save $200 by paying via bank transfer\" lands better than \"2.5% processing fee added for card payments.\" Same math, completely different reaction."

For corporate clients who have to use company cards, just build the fee into your base pricing. Their accounting departments expect it, and nobody's going to push back on a line item that's industry standard.

4. Optimize payment methods by event type

Different events have genuinely different payment preferences. Worth mapping them out explicitly:

| Event Type | Preferred Payment | Fee Strategy |

|---|---|---|

| Corporate events | Company cards | Build fees into base pricing; net terms for regulars |

| Wedding/social | Flexible | Card for deposits, ACH for final balance |

| Nonprofit/charity | ACH strongly preferred | Max discount for ACH; sometimes absorb fees as goodwill |

Build payment method defaults into your booking system by event type. Otherwise staff will default to whatever's easiest, and you'll leave fee-saving options on the table constantly.

5. Renegotiate merchant account terms

The settlement reshapes the processing landscape. Your current processor may not automatically pass through the interchange savings — you have to ask.

Contact them and request:

-

Confirmation that interchange reductions will be passed through to you

-

A review of your current markup rates against post-settlement market rates

-

Removal of any unnecessary monthly fees

If they push back, shop around. Processors are working harder to retain merchants right now, and that's real leverage. Also worth looking at newer platforms built for high-ticket B2B transactions — some offer effective rates under 2% for ACH-like payment methods that clear in one to two business days, which suits catering deposits well.

6. Build fee impact into menu engineering

Buffet service (typically lower margins): More sensitive to payment fees eating into already-thin margins. Prioritize cash/ACH incentives and set minimum order sizes that justify transaction costs.

Plated service (higher margins): Can absorb fees more easily. Build into base pricing and focus on total event profitability rather than per-transaction costs.

Corporate lunch delivery (high volume, low margin): Payment fees can genuinely destroy profitability here. Require ACH for regular accounts and set minimums that actually cover transaction costs — otherwise you're quietly losing money on every order.

The workflow automation opportunity

Manual payment tracking and fee optimization is tedious. This is where AI-powered operational software earns its keep — not as some magic solution, but as a practical tool for capturing fee data and automating routine decisions.

A well-configured booking platform can automatically calculate effective payment rates per transaction, flag events where fees are running above target, suggest optimal payment schedules based on invoice size, and generate fee-adjusted proposals with both payment options laid out clearly. Modern platforms with AI automation handle this kind of workflow optimization without much fuss — the key is connecting payment data to your broader operational metrics so processing costs tie directly into event profitability and pricing decisions. Without that connection, you're still flying blind even with good tools.

Automate flagging for events where effective rates exceed your target so sales can intervene before proposals are finalized.

The settlement creates a window where caterers actively reviewing their payment operations have a real edge. While competitors let the fee reduction get absorbed without thinking about it, there's an opportunity to capture those savings and put them somewhere useful.

Playing the long game with payment strategy

The Visa/Mastercard settlement is one data point in a broader shift. Payment rails are evolving — real-time payments, B2B-focused platforms, embedded finance options are all moving fast. Caterers who build more flexible payment operations now will adapt more easily to whatever comes next.

Beyond processing fees, start thinking about:

-

Working with corporate clients on preferred payment methods that work for both sides

-

Exploring industry-specific payment platforms built for high-ticket event businesses

-

Testing digital wallet options for smaller add-on charges

-

Building payment terms into how you pitch against competitors

The caterers who win long-term aren't necessarily the ones with the lowest processing fees. They're the ones who understand their payment costs well enough to make deliberate choices — knowing when absorbing fees wins a contract, when passing them through makes sense, and when offering an ACH discount is worth the conversation.

Moving forward with payment optimization

The swipe fee settlement is an inflection point. That 0.1% reduction looks small, but across hundreds of events annually it represents real recovered margin. And the surcharging rule changes open up pricing strategies that weren't previously on the table.

Capturing any of that requires more than waiting for lower fees to show up on a statement. It takes granular tracking, strategic payment scheduling, honest pricing options, and the discipline to apply them consistently.

Start simple: pull the last three months of processing statements and calculate your effective rate by event type. Build that visibility into your operational tracking. Then work through the six moves above, testing what fits your client mix.

Caterers treating payment processing as an unavoidable cost of doing business will keep bleeding margin quietly. In a business where 3% to 5% net margins are considered solid, recovering even half a percentage point from payment optimization can be the difference between breaking even and actually building reserves. The settlement handed you an opening — whether you build the operational infrastructure to use it is a different question entirely.

Ready to elevate your catering business?

Join 500+ caterers trusting Caterngly to save time, reduce errors, and deliver flawless events.